The interest of investors in ESG (environmental, social, and governance) products is growing very rapidly, but the lack of standard information can be very frustrating. The definition of what counts as sustainable often seems arbitrary: for example, S&P Global’s recent decision to drop electric car manufacturer Tesla from its ESG index has sparked a big controversy – leading Tesla CEO Elon Musk to call ESG “a scam”. Admittedly, this decision is very surprising, considering that this index includes ExxonMobil, the largest oil and gas company in the world.

This controversy suggests that ESG, and sustainability in general, may be very difficult to reduce to a single dimension. How can an ESG rating system conclude that an oil and gas company is more sustainable than an electric car manufacturer? More generally, can elements as diverse as efforts to reduce the gender pay gap, compliance with labor rights, or greenhouse gas emissions all be summarised in one unique score?

In order to close the information gap about ESG, the European Union has started to implement the Sustainable Finance Disclosure Regulation (SFDR). This piece of legislation aims at improving the quality of extra-financial reporting by investment firms, so that end investors may better understand how they take sustainability risks into account. To do that, it introduces new sustainability requirements and criteria, so that financial products may be compared with one another with more relevance.

In short, this legislation aims at avoiding “greenwashing”, i.e. at preventing investment funds from marketing their financial products as ESG without being fully transparent about their actual exposure to sustainability risks.

This new legislation will therefore improve the quality of extra-financial information on financial products, but it will also pose challenges for investment firms. Here are the key points financial institutions have to have in mind from now on.

Who is it for?

SFDR targets all “financial market participants” that are based in the European Union. This category is defined within the regulation itself (article 2), and it essentially includes companies that invest money on behalf of their customers or other stakeholders: asset managers, fund managers, providers of pension products… as well as venture capital or private equity funds. This regulation targets all financial market participants, even when they do not claim to have sustainable financial products.

In addition to that, the European Commission has confirmed that SFDR has extraterritorial effects since it also targets financial market participants that are located outside of the EU, but that market their products in the EU.

What does it change?

The SFDR regulation introduces two main categories of requirements:

sustainability reporting requirements,

additional demands on the transparency of financial products.

Reporting standards

The goal of SFDR is to improve the quality of information available to investors on sustainability topics. As such, it adds new reporting requirements.

More precisely, under this legislation, you are expected to publish and update information on your website about your level of integration of sustainability risks. This includes the following items:

How are these risks taken into account in the decision-making process?

What impact may these risks have on the returns of the financial products?

How are your remuneration policies aligned with the integration of sustainability risks?

If your firm is in the scope of SFDR, then this requirement is mandatory, regardless of your size.

In addition to that, if your firm has 500 employees or more, then you must communicate Principal Adverse Impacts (PAIs), which means the effects that your investments may have on the environment. If your company is below this employee size, this step becomes optional; however, if you choose not to report, you need to communicate on why this piece of reporting is not applicable.

The ESAs have updated the list of indicators for Principal Adverse Impacts. The principal adverse impact reporting in the SFDR is based on the principle of proportionality – for companies with fewer than 500 employees, the entity-level principal adverse impact reporting applies on a comply-or-explain basis.

Source: EIOPA

Principal Adverse Impacts cover all three pillars of ESG, with 18 indicators – of which 8 are related to climate and greenhouse gas emissions. This is very revealing about the importance of climate in the European Commission’s sustainability agenda.

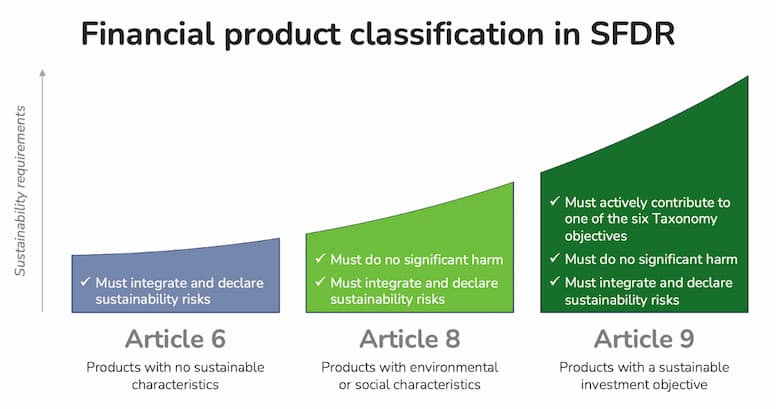

Funds classification

The second type of obligation aims at standardising what qualifies as a sustainable financial product: for this reason, it is particularly relevant if at least one of your investment funds is marketed as a sustainable product.

SFDR makes the distinction between three types of financial products, with varying degrees of sustainability expectations and requirements.

Article 6 corresponds to financial products which do not take into account sustainability criteria in the investment process (“not-at-all green”).

Article 8 (“light green”) covers financial products which promote “environmental or social characteristics”.

Article 9 (“dark green”) applies to products that have sustainable investment as their objective.

Financial products may therefore fall under any of those three categories, according to their sustainability ambitions: the more sustainable, the more demanding the standards. If none of your products are marketed as sustainable, then there are no additional specific requirements, aside from the reporting standards mentioned above.

However, if at least one of your financial products is sustainable (article 8 or 9), then you must also make sure that they “do no significant harm” to any of the six objectives defined by the EU Taxonomy Regulation:

Climate change mitigation

Climate change adaptation

The sustainable use and protection of water and marine resources

The transition to a circular economy

Pollution prevention and control

The protection and restoration of biodiversity and ecosystems

You must also confirm that your investments comply with the OECD Guidelines for Multinational Enterprises, as well as the UN Guiding Principles on Business and Human Rights.

In addition to that, if some of your products are “dark green”, then you must establish how they actively contribute to at least one of the six objectives outlined in the Taxonomy Regulation.

When does this apply?

The implementation of SFDR will occur in two phases. The first one, called “Level 1”, has been in effect since March 2021: since the publication of the technical documentation was delayed, it works in a principle-based manner, i.e. companies are expected to comply with the regulation on a high-level basis, with no precise standards set for reporting.

The level 2 phase went live in January 2023 and integrates the Regulatory Technical Standards (RTS), which gives the full set of rules about how companies are expected to comply with the standard. These new RTS also add reporting templates for Principal Adverse Impacts and for sustainability disclosure about financial products.

Specifically, starting in January 2023, financial institutions have to communicate every year about their integration of sustainability risks, Principal Adverse Impacts indicators, and the level of sustainability of their products in their annual report. This communication should be done using the templates created by the European Commission.

Conclusions

The implementation of SFDR will bring additional transparency to the end investors, but financial market participants may find it difficult to comply with this regulation: in particular, collecting data about investee firms may be a real challenge. This is especially true for the smallest portfolio companies since extra-financial reporting is not mandatory for them.

Financial market participants have a lot at stake on these topics. Because of the increasing pressure for a green transition, sustainability risks and Principal Adverse Impacts are turning into financial risks: investing firms who do not take them into account correctly could end up being in danger. There are also significant opportunities in the field, as assets in Article 8 and Article 9 funds reached EUR 4.05 trillion at the end of December 2021, representing 42.4% of all funds sold in the EU.

Sources

Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability‐related disclosures in the financial services sector. Available at: 02019R2088-20200712 – EN – EUR-Lex

Annexes 1 to 5 of the Regulatory Technical Standards, are available at this link.

United Nations, Guiding Principles on Business and Human Rights

Morning Star, SFDR Article 8 and Article 9 Funds: 2021 in Review https://www.morningstar.com/en-uk/lp/sfdr-article8-article9