Sustainability objectives have grown to be a central concern for European Union (EU) governments in recent years, aiming to encourage capital to flow to projects promoting a more sustainable economy.

A key component of the EU Sustainable Finance Action Plan is the Sustainable Finance Disclosure Regulation (SFDR). Several other regulations followed and the European Taxonomy Regulation is one of them.

These regulations establish specific social and environmental criteria that investment-related activities must meet. As such, the stakes of the SFDR for investment funds are important and need to be considered carefully.

Follow Carbometrix’s guide to get to know all about these new regulations and their impact on funds.

Key information

The SFDR regulation was introduced to improve the transparency and comparability of European financial products in terms of social, environmental, and governance sustainability. All actors in the European financial market are hence affected by this regulation.

Asset managers and advisors are required to provide specific information on their assets’ sustainability risks and their main detrimental effects (Principal Adverse Impact).

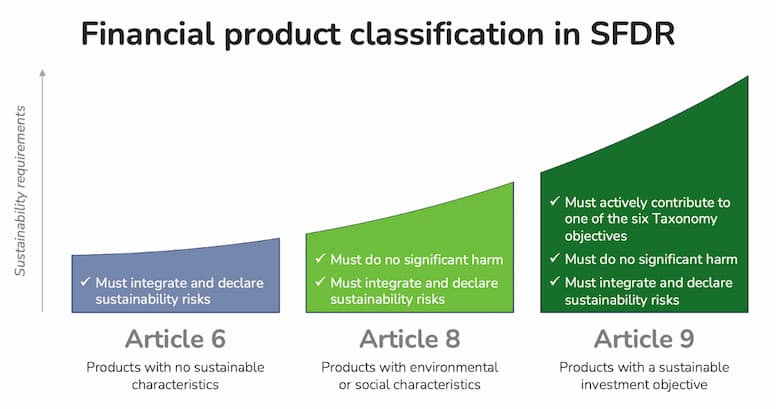

Investment funds are ranked according to 3 levels of commitment to sustainability: Article 6, Article 8, or Article 9. The more committed the fund, the higher the corollary requirements.

Why was the SFDR enacted?

Opacity on firms’ real ecological commitment

The European Union is increasingly tackling greenwashing and its problems. Indeed, the communication and marketing of firms on their sustainable commitment is perhaps misleading, sometimes even false. The reality of their ecological commitment is therefore particularly difficult to determine.

Until now, investment funds required very little information and transparency from the firms in which they invested.

The existing Environmental, Social, and Governance (ESG) criteria lacked transparency and did not allow for qualitative comparisons between companies. For example, the electric car manufacturer Tesla was removed from the S&P Global ESG list, while ExxonMobil, the world’s largest oil and gas company, is – as of today – still included.

Obsolete criteria

Introducing new criteria to qualify the real commitment of companies seemed inevitable. Thus, it became necessary to implement more transparent and understandable criteria and to allow for better comparability of activities.

This is how the SFDR regulation was born. Complemented by other regulations such as the European Taxonomy Regulation, it sets out new criteria to qualify the environmental commitment of firms and investors.

The SFDR is designed to redirect capital flows toward more sustainable growth and to help investors make better financial choices. As a whole, its ultimate goal is to support the transition of the European financial system towards a more sustainable economy.

Who does the SFDR regulation concern?

This regulation targets all agents and advisors in the EU financial markets, i.e. asset managers and firms investing in them on behalf of their clients or other stakeholders. To this extent, this even affects participants who do not claim to sell sustainable products!

The regulation also applies to financial agents and advisors outside the EU, but who aim their production at European markets, according to Article 2 of the SFDR.

The regulation concerns the following financial products:

UCITS (Undertakings for the Collective Investment in Transferable Securities);

AIFs (Alternative Investment Funds)

Separately managed portfolios;

Financial advice (provided in the EU or by an EU investment firm).

What are the SFDR’s fundamentals?

New requirements for sustainability reporting

The SFDR regulation changes EU reporting requirements on the sustainability of the activities of agents on the European financial market.

The latter are now required to publish and update information on their websites regarding their level of integration of sustainability risks.

These risks enclose environmental, social, or governance conditions (such as climate change) which have or could have negative externalities on the value of an investment.

Principal Adverse Impacts

On top of the requirement to publish such information, the negative impact of investment decisions or advice on sustainable development must be taken into account. This is known as Principal Adverse Impact (PAI).

European financial market participants are now required to disclose how they take into account their investment decisions’ negative externalities on the environment and social justice.

Where appropriate, they must also reveal how this translates into each of their financial products.

To support actors in their reporting, regulators have introduced Regulatory Technical Standards (RTS). These provide guidance on the content, method and presentation of the relevant information to be disclosed.

A new classification of investment funds according to their commitment to sustainability

The SFDR regulation also updates standardisation regulations on the qualification of a sustainable financial product. Financial products are now classified into 3 categories: Article 6, Article 8 or Article 9.

Article 6 products have no sustainability objectives.

Article 8 covers financial products with certain social or environmental features.

Article 9 covers those considering sustainability as a main objective for their investments.

Financial product classification in SFDR under Articles 6, 8 and 9

European financial products are classified in one of the above categories. The regulatory requirements that apply to them increase with their degree of commitment to sustainable development.

Clearly, financial products have much to gain from being classified under Articles 8 or 9. However, the greater the commitment to sustainability, the more demanding the criteria that must be met by these financial products.

Article 6 products have no obligations other than to incorporate and disclose sustainability and climate change risks, see above.

Articles 8 and 9 products must also demonstrate that they do not significantly undermine any of the 6 objectives of the EU Taxonomy Regulation. In addition, products under Article 9 qualification must prove that they actively contribute to one of the 6 criteria given below.

The 6 aims of the European Taxonomy Regulation:

Climate change mitigation

Climate change adaptation

Sustainable use and protection of water and marine resources

Transition to a circular economy

Pollution prevention and control

Protection and restoration of biodiversity and ecosystems

The 6 aims of the EU Taxonomy Regulation

Article 8 financial products must demonstrate that they do not undermine any of these objectives. Article 9 financial products must show how they actively contribute to at least one of the latter.

You are an asset manager for products under Article 8 or 9 regulations, what are your obligations?

The implementation of these new regulations is a two-stage process. The first stage (level 1) started in March 2021. The second stage (level 2) will start in January 2023. Find out more below.

Level 1

In March 2021, EU legislators published the first documents in regard to SFDR measures. Financial market participants are now required to broadly comply with the above-mentioned regulations, without having to meet specific reporting standards. Agents subject to the SFDR must:

Disclose their sustainable investment strategy, relative to the products concerned and the associated management firm;

Describe how they plan to integrate sustainability risks into their investment decisions.

Level 2

From 1st January 2023, financial actors will be required each year to:

Describe how they integrate sustainability risks into their products;

Include the Principal Adverse Impact indicator to their report in detail;

Determine the level of sustainability of their products (Articles 6, 8 or 9) and take appropriate action.

Here are a few examples of the topics included in the disclosure obligation for investment funds under Articles 8 or 9:

Disclosure of the key elements of their investment strategy and to what extent they achieve the fund’s stated environmental or social sustainability goals;

Clarification of the investment strategy, indicating the risk factors and aimed goals;

Evidence that investments are not detrimental to social and environmental sustainability and are consistent with the OECD Sustainable Development Goals (SDGs);

Evidence of non-detrimental compliance (for Article 8 funds) or active participation (for Article 9 funds) to the objectives of the European Taxonomy Regulation.

For more information on the SFDR regulation, visit EUR-lex’s website on SFDR regulations. To find the EU templates created by regulatory instances to report this information, visit this website.

Data: a crucial challenge for SFDR regulations

Investment funds have a responsibility to demonstrate their commitment to sustainability in a transparent and standardised way. Funds now have a new major challenge to consider: data collection.

Funds are required to provide a certain amount of claims about the sustainability of the companies in which they invest. The challenge for funds is thus to find an efficient way to collect data, in a timely manner.

Such data encompass data from management firms (such as extra-financial performance or sustainability risks) and financial products (also including sustainability risks or their impact and compliance with RTS criteria).

Some of the information to be published requires data that does not yet exist or that companies will only be required to collect from next year. The challenge is even greater for smaller firms, not yet compelled to publish extra-financial data. Even today, some pieces of information are not always disclosed by the firms in which funds invest.

All assets aligned with the European Taxonomy will henceforth require systematic information disclosure by firms. This will most probably require a significant effort of them, at least at first.

Conclusion

The updated SFDR rules that will be applied in January 2023 require genuine anticipation from investment funds. Depending on the classification of their commitment to sustainable development (i.e., Articles 6, 8 or 9), the obligations they must face are more or less demanding. Funds need to justify this level of commitment by proving that their strategy is aligned with the EU’s sustainability objectives.

It is therefore essential for financial agents to address their compliance with the SFDR. This includes identifying the climate risk exposure of their assets and measuring their carbon impact. Where appropriate, this also includes measuring their degree of mitigation or participation in the climate change transition.

Funds are now also required to define a clear path to ensure their assets’ ecological performance. This path must be designed to meet aims set, while at the same time meeting those of the SFDR. Carbometrix can assist you in implementing SFDR through a rigorous calculation of your climate-related PAIs (Principal Adverse Impacts).